Chatbots for Banking: A Guide for SMBs & Credit Unions

A practical guide to chatbots for banking. Learn use cases, security best practices, and how to choose a vendor for your SMB bank or credit union.

By 2022, over 98 million people in the U.S. had already interacted with a bank chatbot, representing about 37% of the population, and the Consumer Financial Protection Bureau projected that figure would reach 110.9 million by 2026. The same report noted that each of the top 10 largest commercial banks had already deployed chatbots in customer service (CFPB research on chatbots in consumer finance).

For a credit union or community bank, that changes the conversation. Chatbots for banking aren't a digital novelty anymore. They're part of the service baseline customers already see elsewhere, especially when they need a balance, transaction history, card help, or a quick answer outside branch hours.

The primary question for smaller institutions isn't whether to copy a national bank feature set. It's how to implement conversational banking in a way that fits tighter budgets, leaner teams, and a higher sensitivity to security, compliance, and member trust.

Table of Contents

- Why Chatbots for Banking Are No Longer Optional

- Key Use Cases Driving ROI in Banking

- Designing Conversations That Build Customer Trust

- Integrating Your Chatbot with Core Banking Systems

- Managing Security and Compliance in Conversational Banking

- How to Choose the Right Banking Chatbot Vendor

- Measuring Chatbot Success and Calculating ROI

Why Chatbots for Banking Are No Longer Optional

Large banks reset service expectations years ago. Members now expect answers in seconds, outside branch hours, on the same channels they use for everything else.

For a community bank or credit union, that shift creates a practical problem. Every routine balance question, card-status check, or fee inquiry that lands in the contact center adds cost, wait time, and pressure on staff who should be handling higher-value work. Institutions that leave these requests to phone queues and branch callbacks are asking members to accept a level of friction they no longer tolerate.

The priority is not building an enterprise AI program from scratch. The priority is covering the service gaps that members feel first, with a scope your team can support.

For SMB banks and credit unions, the case is straightforward:

- Extend service coverage without adding headcount. Member questions do not stop after business hours.

- Cut low-value contact volume. Repetitive, low-risk requests should not consume trained staff time.

- Protect staff capacity for complex work. Lending discussions, fraud cases, and retention conversations need people.

- Stay competitive on convenience. Smaller institutions rarely outspend national banks, but they can remove delay in common service interactions.

Practical rule: If a request is frequent, rules-based, and low-risk, the bot should probably handle it.

The technology has also improved. As noted earlier, banking chatbots are no longer limited to rigid decision trees and keyword matching. Customers now judge the experience against the best digital service they receive anywhere, whether that comes from a national bank, a retailer, or a software platform. An FAQ-style bot that fails on plain-language questions does not lower service cost. It adds another dead end.

That is why a phased rollout works better than a broad launch. Start with a narrow set of service requests, put clear escalation paths around anything sensitive, and prove that the bot can reduce volume without increasing risk. For smaller institutions with tight budgets and lean technical teams, that is the workable path. It keeps the project affordable, gives compliance and operations teams time to build confidence, and creates a real business case for expansion.

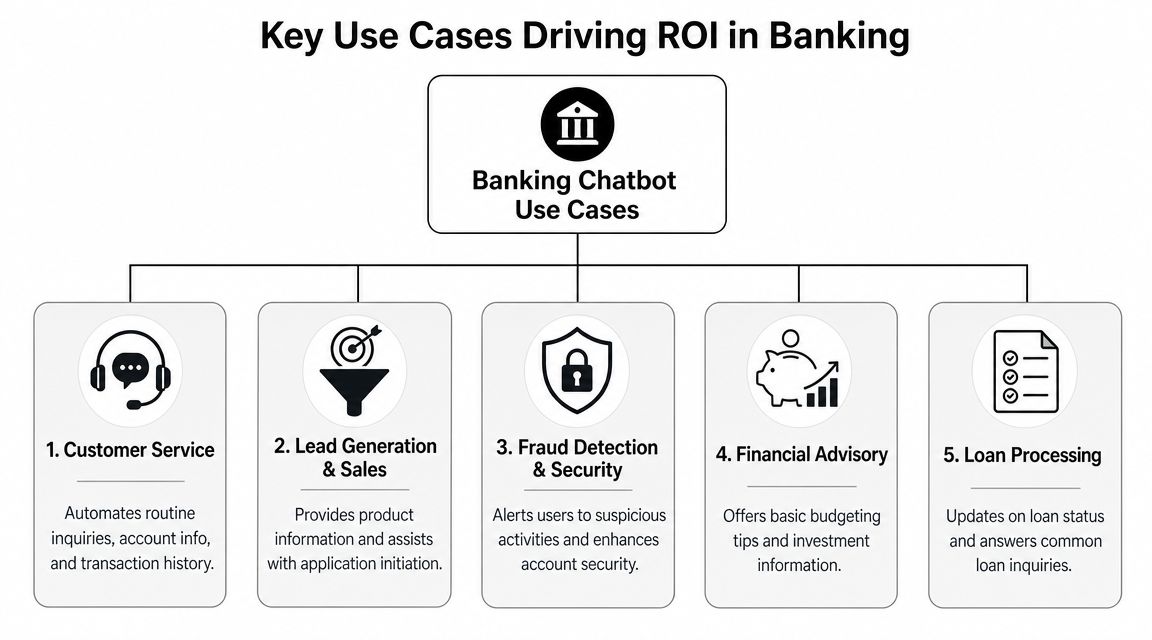

Key Use Cases Driving ROI in Banking

The strongest chatbot programs don't begin with a broad promise to “transform service.” They begin with a handful of high-volume workflows that already create friction for members and cost for the institution.

Start with repetitive service demand

Chatbots for banking often prove their value most quickly. In production deployments, one industry source reports that AI chatbots can handle 80–90% of queries and cut call-center costs by up to $1.2M per year, while another says banks can automate around 90% of client relations (Master of Code coverage of banking chatbot operations).

For a smaller institution, that doesn't mean aiming for maximum containment from day one. It means identifying the interactions that show up every week and consume staff time without requiring nuanced judgment.

Typical starting points include:

- Balance and transaction history requests. These are frequent, predictable, and easy to structure.

- Debit card support. Lost card guidance, card status questions, and basic next-step instructions fit well.

- Fee and account questions. Members often need quick clarification, not a long conversation.

- Loan and payment status checks. Many inquiries are informational rather than advisory.

- Branch and digital banking help. Login guidance, routing to the right form, or app support can be standardized.

A good test is simple. If a branch manager hears the same question repeatedly, the bot should probably answer it.

Later in the member journey, the same chatbot can help with product discovery and intake. It can explain account options, collect preliminary information for a loan inquiry, or guide a visitor toward the right form without turning the conversation into a hard sell.

Here's a short walkthrough of how banks are approaching these use cases in practice:

Use the bot to support growth, not just deflect tickets

A common mistake is treating the chatbot as a cost-cutting shell around the contact center. That leaves value on the table.

A stronger approach uses the bot to improve conversion and completion in common member journeys:

| Use case | What the chatbot does | Business outcome |

|---|---|---|

| New account inquiries | Explains products and routes to the right application path | Fewer abandoned journeys |

| Loan pre-screening | Collects basic intent and qualification details | Better handoff to lending staff |

| Payment and servicing questions | Reduces confusion during active account management | Lower inbound service pressure |

| Fraud alerts and status guidance | Gives immediate next steps and routes urgent cases | Faster member reassurance |

The key is restraint. A chatbot should support product education and intake, but it shouldn't pretend to provide complex financial advice or make sensitive decisions conversationally unless the workflow is tightly controlled.

Don't ignore internal employee use cases

This is one of the most overlooked areas for SMB banks and credit unions. Internal bots can help staff find policies, procedures, HR information, IT support steps, and operational guidance without searching across scattered PDFs, intranet pages, and old email threads.

One industry analysis describes internal AI chatbots for employees as a “very strong and often underestimated” direction, especially as chatbot systems evolve into a workflow and knowledge layer across the bank (Lumitech analysis of AI chatbots in banking).

The quickest win is often not member-facing. It's helping frontline staff get the right answer faster and more consistently.

For smaller institutions, that internal use case can be easier to launch than a transactional member bot. It has fewer external risks, clearer content boundaries, and a direct effect on service consistency across branches and contact center teams.

Designing Conversations That Build Customer Trust

A banking chatbot fails long before the model fails. It fails when the interaction feels evasive, confusing, or indifferent at the exact moment the customer needs confidence.

MIT Sloan argues that AI cannot provide critical human financial-service capabilities such as empathy, judgment, and ethics, and industry commentary has noted that many bank bots still function more like search tools than real problem-solvers (MIT Sloan on the human financial-service activities AI can't do). That's not an argument against automation. It's an argument for designing boundaries.

Trust starts with clarity, not personality

Some teams spend too much time making the bot sound friendly and not enough time making it useful. In banking, trust comes from clear language, accurate options, and predictable next steps.

The basics matter:

- State what the bot can do. If it can help with balances, card support, and loan status, say so upfront.

- Use plain banking language. Members shouldn't have to decode internal terminology.

- Confirm actions before they matter. If the user is about to request something sensitive, the bot should slow down and verify intent.

- Avoid bluffing. If the bot doesn't know, it should say so and hand off.

A credit union voice can still feel human without becoming casual. Friendly is good. Vague isn't.

Design for the moments when automation should stop

Urgent and emotionally charged situations are where poor chatbot design does the most damage. Suspected fraud, disputed charges, lost cards while traveling, payment hardship, or a frozen account all require more than efficient intent detection.

In those moments, the bot should recognize signals that the conversation has crossed from service to risk or distress. That means routing fast, preserving context, and not forcing the member to repeat information.

A practical escalation design usually includes:

- Trigger phrases and scenarios tied to fraud, hardship, disputes, or account access failure.

- Immediate acknowledgment that the issue may require a specialist.

- Minimal additional questioning before handoff.

- Visible routing options such as secure messaging, call-back, or live agent transfer.

- Conversation summary transfer so the human team starts informed.

A high containment rate can look efficient on a dashboard and still damage trust if the bot traps people in the wrong conversations.

For leadership teams, this is a policy choice as much as a UX choice. Decide in advance which interactions should never be over-automated. Then make those rules visible in the design, not buried in project notes.

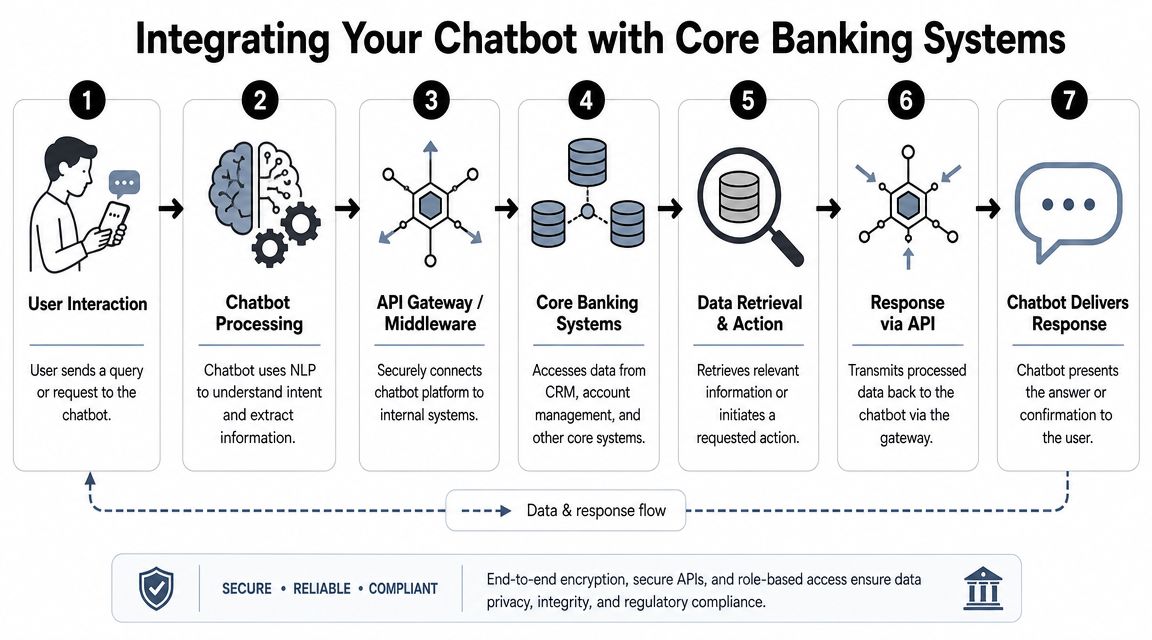

Integrating Your Chatbot with Core Banking Systems

A banking chatbot becomes useful when it moves beyond general answers and can securely retrieve real account information or trigger approved actions. Without integration, it's a brochure. With the right integration model, it becomes a controlled digital service channel.

Treat the bot like a digital teller with limited permissions

The cleanest way to explain architecture to a leadership team is this: the chatbot should act like a digital teller with specific permissions. It shouldn't have broad, uncontrolled access to the core. It should be allowed to do a defined set of things, through approved interfaces, under clear rules.

In practice, that usually means the chatbot connects to:

- Core banking APIs for balances, transaction history, and account-level data

- CRM or service systems for customer context and case history

- Knowledge bases for policy answers, product information, and procedures

- Authentication layers that verify who the user is before any protected information is returned

That middle layer matters. The bot should rarely talk directly to every backend system on its own. A gateway or middleware layer gives the institution a place to manage permissions, logging, routing, and security policy.

If your team is also mapping customer context across service systems, this guide to chatbot CRM integration is a useful reference point for how conversation history and customer records should work together.

A practical integration roadmap for smaller institutions

Most SMB banks and credit unions shouldn't start with transactional complexity. Start with a staged rollout.

| Phase | What to connect | What the bot should do |

|---|---|---|

| Phase 1 | Knowledge base and public content | Answer FAQs, branch info, product basics |

| Phase 2 | Authentication and account data APIs | Provide balances, history, and servicing info |

| Phase 3 | CRM and case systems | Personalize support and improve handoff |

| Phase 4 | Selected action workflows | Handle approved requests under stronger controls |

That sequence lowers risk and shortens time to value. It also helps the institution test content accuracy, escalation quality, and operational ownership before exposing more sensitive functionality.

A few implementation rules help:

- Limit the first release. Don't launch with every intent the vendor demo showed.

- Map every answer to a source system. If nobody owns the underlying content, the bot will drift.

- Define failure handling early. The user needs a clean path when an API times out, data is missing, or authentication fails.

- Keep service and IT aligned. The best conversational flow still fails if backend access is brittle.

The institutions that do this well don't chase the most advanced demo. They build a controlled service layer that can expand over time.

Managing Security and Compliance in Conversational Banking

Security concerns are usually the point where a chatbot project either matures or stalls. That's healthy. In financial services, skepticism is useful. The goal isn't to make leadership comfortable with vague assurances. It's to show how conversational access can be controlled like any other channel.

Separate low-risk requests from high-risk actions

Independent banking guidance recommends designing chatbot integrations around core-banking API access for balances and histories, while restricting higher-risk actions with multi-factor authentication, biometric verification where feasible, and session security controls. The same guidance recommends end-to-end encryption, continuous fraud-detection integration, and immutable audit trails for every interaction (AiMultiple guidance on banking chatbot security).

That creates a practical policy model:

- Low-risk informational requests can sit behind lighter controls once the user is appropriately recognized in a secure session.

- Higher-risk actions need stepped-up authentication and stronger session checks.

- Regulated or exception-heavy workflows often belong with a human reviewer even if the chatbot initiates the process.

Many smaller institutions go wrong. They treat “chatbot” as one risk category. It isn't. A balance inquiry and a sensitive account action do not deserve the same control model.

Build controls into the conversation layer

Compliance doesn't live only in the backend. The conversation itself needs guardrails.

That includes:

- Authentication gates before protected data is revealed

- Session timeouts and session continuity rules

- Redaction policies for sensitive fields in logs or transcripts

- Fraud signals that trigger secondary verification or escalation

- Auditability so reviewers can see what the bot showed, asked, and executed

A useful working standard is this: if the institution can't reconstruct the interaction later, the control design is incomplete.

For teams reviewing platforms, this broader AI chatbot security and data privacy guide is a practical checklist for evaluating how vendors handle data flow, storage, and access controls.

Risk checkpoint: Every chatbot action should have an owner, a log trail, and a clear authentication requirement.

Governance matters as much as technology

Most compliance issues in chatbot projects come from weak governance rather than weak models. Content gets outdated. Escalation rules are unclear. Vendors are approved before the bank decides which data can enter the system. Customer-facing scripts drift away from policy.

A stronger operating model assigns ownership across four lanes:

- Business owner for use cases and customer experience

- IT owner for integration, identity, and environment controls

- Compliance and risk owner for approved workflows and review criteria

- Operations owner for transcript review, tuning, and escalation performance

That sounds heavy, but for a small institution it can be lean. The important part is clarity. If everyone assumes someone else owns the bot, no one really does.

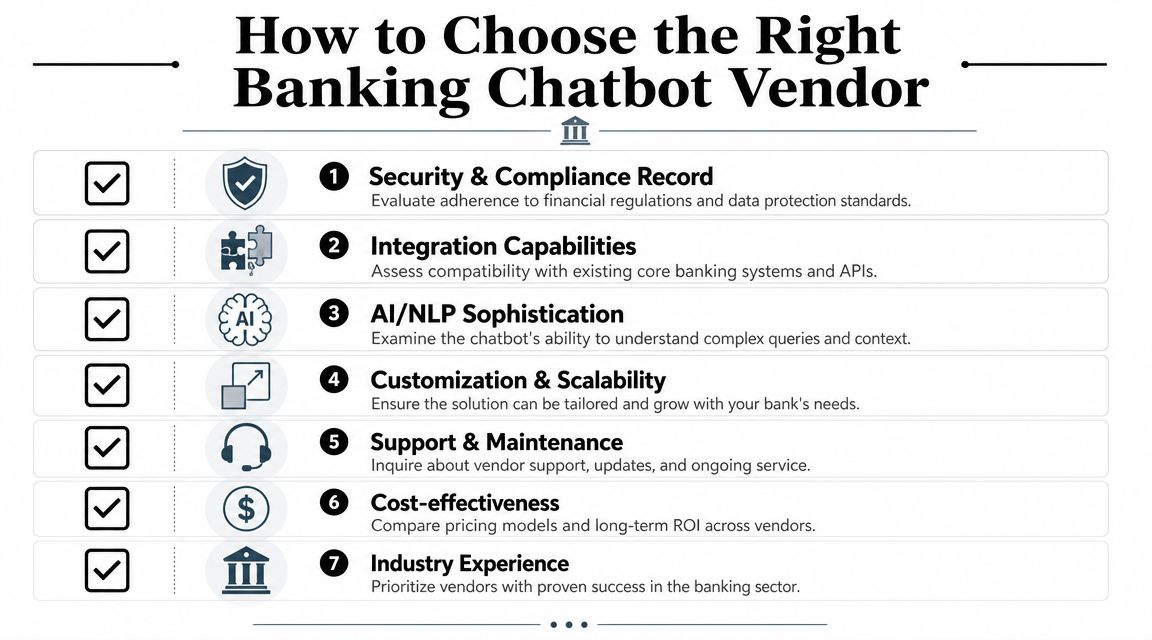

How to Choose the Right Banking Chatbot Vendor

A weak vendor choice usually shows up six months after launch. The pilot works, but the integration stalls, staff cannot maintain content without vendor support, and compliance review turns into a bottleneck. For SMB banks and credit unions, the better decision is usually the vendor that fits your operating model, budget, and control requirements from day one.

Build a shortlist around implementation reality

Start with a small shortlist. Three to five vendors is enough if the screening criteria are practical.

For community banks and credit unions, I recommend evaluating vendors in the same order the project will succeed or fail. First, confirm the platform fits your control environment. Next, confirm it can connect to the systems you already run without a long custom build. Then assess whether your internal team can manage it after go-live.

Use five filters early:

- Control fit. Can the platform support your approval process, authentication boundaries, and data handling rules without workarounds?

- Integration path. Is there a credible plan for connecting to your core, CRM, knowledge base, and ticketing tools in phases?

- Operational workload. Can business and operations teams update content, review conversations, and adjust routing without depending on engineers for routine changes?

- Channel fit. Does the vendor support the channels you need now, with a realistic path to add others later?

- Pricing model. Can leadership understand how costs change with usage, new channels, and added workflows?

That phased view matters. Small institutions rarely need every capability in phase one. They do need a vendor that can start with lower-risk service use cases, then expand into authenticated workflows without forcing a platform change 12 months later.

One option some smaller teams consider for no-code, multi-channel deployment is Hyperleap AI. It supports website and messaging channels, document-grounded responses, and unified inbox workflows. For a banking use case, ease of setup should not outweigh clear integration boundaries, admin controls, and a realistic operating model. Teams building the business case should also review a chatbot ROI framework for business cases and rollout planning before comparing vendors on price alone.

Questions leadership should ask every vendor

A polished demo is not enough. The buying team should test whether the vendor can support day-two operations, not just day-one excitement.

| Question | Why it matters |

|---|---|

| How do you handle authentication before sensitive responses? | Distinguishes basic FAQ tooling from platforms that can support banking workflows |

| What systems have you integrated with in similar institutions? | Shows whether the implementation plan is proven or theoretical |

| How are transcripts logged, retained, and reviewed? | Supports oversight, issue investigation, and internal review |

| How do human handoffs work? | Service quality depends on fast, accurate escalation |

| Who updates content and how quickly? | Policies, rates, and service rules change often |

| What happens when the bot is uncertain? | Safe fallback behavior protects trust and reduces avoidable risk |

Ask for specifics. Which core systems? Which identity tools? Which channels are native, and which require partners or custom work? Vague answers usually mean more cost and delay later.

One more practical step helps. Ask to see the admin console, approval workflow, reporting, and conversation review tools. That is where your operations, digital banking, and service teams will spend their time after launch.

Measuring Chatbot Success and Calculating ROI

If leadership only asks whether the chatbot is “working,” the program will drift toward vanity metrics. Success in banking needs to connect operational performance to cost, service quality, and member retention.

A forecast cited in banking-industry coverage said banks were expected to spend $9.4 billion on AI chatbots in 2025, and the same coverage referenced a survey reporting that chatbots can handle 80–90% of bank client requests without human intervention (banking chatbot investment and handling statistics). That level of investment tells you something important. Institutions aren't funding chatbots as novelty software. They're funding them as an operating layer.

Track operational metrics that connect to cost and service

For a credit union or SMB bank, the useful KPIs are usually straightforward:

- Containment rate. How many conversations end without human intervention, but only for the right types of requests.

- Escalation quality. Did the handoff happen fast enough, with enough context, in the right scenarios?

- Resolution time. Are routine requests getting solved faster than they were before?

- Deflection by intent. Which high-volume request types are no longer reaching staff?

- Customer feedback. Did members feel helped, especially in low-stakes interactions?

The discipline is to interpret these together. A rising containment rate with poor escalation quality is not a success story.

For teams building the financial model, this AI chatbot ROI framework is a practical way to structure costs, savings assumptions, and rollout stages into a business case leadership can review.

Build the business case in plain language

The strongest ROI cases usually combine three buckets of value:

- Service efficiency, such as reduced repetitive contact volume.

- Staff productivity, especially when frontline and support teams spend less time searching and triaging.

- Revenue support, where the bot improves intake, routing, and completion for product inquiries.

Keep the first phase honest. Don't promise strategic transformation in quarter one. Promise that the institution will automate a defined set of low-risk requests, improve after-hours responsiveness, and give staff cleaner escalation workflows. If that works, expansion becomes much easier to justify.

If your team is evaluating conversational workflows and wants a practical, no-code platform for multi-channel support, Hyperleap AI is one option to review. It lets teams launch document-grounded chatbots across website and messaging channels, manage conversations in a unified inbox, and maintain on-brand responses without a heavy development lift. For banks and credit unions, the right next step is usually a narrow pilot with clear controls, clear ownership, and a defined success scorecard.