Chatbots in Banking: A Complete 2026 Guide

Explore the complete 2026 guide to chatbots in banking. Learn about use cases, benefits, security, deployment, and how to choose the right AI vendor.

By 2026, 110.9 million people in the U.S. are projected to have interacted with a bank's chatbot, according to the Consumer Financial Protection Bureau's research on chatbots in consumer finance. That number changes the conversation. Chatbots in banking are no longer side experiments on a help page. They're part of how banks now deliver service at scale.

For many managers, the confusion starts here. When someone says “banking chatbot,” they might mean a simple FAQ box, or they might mean a secure assistant that can verify a customer, call banking systems, and complete an action. Those are very different tools. Treating them as the same is one reason many projects disappoint.

A useful way to think about it is this: the first generation of bots acted like a directory sign in a branch lobby. They pointed people somewhere else. The newer generation is closer to a digital teller. It can understand what the customer wants, connect to systems, and help complete the job.

Table of Contents

- The New Digital Bank Teller and Why It Matters

- Measuring Success with Core Benefits and KPIs

- Transforming Banking Operations with 5 Core Use Cases

- Understanding Banking Chatbot Architecture and Integration

- Navigating Regulation Security and Customer Trust

- Your Deployment Roadmap and Best Practices

- Choosing Your AI Partner A Vendor Selection Checklist

The New Digital Bank Teller and Why It Matters

Banking chatbots are no longer a pilot project or a website add-on. Large banks already use them at scale because they help solve a basic operating problem: customers ask simple questions all day, while service teams are built to handle a mix of simple and complex work.

That shift matters most when you look past chat as a channel and focus on what the system does. A basic bot answers a question. A stronger one helps a customer complete a task. In banking, that difference is the gap between a digital brochure and a digital teller.

From FAQ bot to transactional assistant

The first generation of banking bots worked like an ATM menu on a website. They were useful for fixed, predictable requests such as branch hours, routing numbers, or card activation instructions. If the customer used the wrong wording, the experience often broke down.

Newer systems are designed to carry more of the service journey. They identify intent, keep track of context across several messages, and connect to bank systems with the right controls in place. So a customer can move from asking, "How do I lock my card?" to initiating that request in the same conversation.

A practical way to frame the progression is:

- FAQ bot: Answers common questions with prewritten responses.

- Conversational assistant: Interprets intent and guides the customer through a process.

- Transactional banking assistant: Connects to core or adjacent banking systems so approved actions can begin or be completed securely.

That progression is the core story. The market is moving from chatbots that deflect contacts to assistants that carry out service work.

Why business owners and bank managers should care

For a bank manager, this changes staffing economics and service design at the same time. Routine requests such as balance checks, payment status questions, password resets, and card controls can be handled around the clock. Human agents then spend more time on exceptions, complaints, fraud concerns, and cases where judgment matters.

For a business owner evaluating banking partners, the value is also practical. If your bank's assistant can answer cash management questions, help locate transaction details, or guide a user to the right treasury workflow without a long hold time, service feels faster even when no branch employee is involved.

The risk is just as practical.

A weak bot creates a new queue instead of removing one. It asks the customer to restate the problem, fails to authenticate cleanly, and hands the case to an agent without context. That is why banks should judge chatbot maturity by task completion, system integration, and handoff quality, not by whether a chat window exists. If you need a framework for that, these AI chatbot KPIs for measuring success provide a useful starting point.

The key question is simple: does the assistant help customers get something done safely, or does it only answer around the edges of the task? In banking, that answer determines whether the chatbot reduces operational pressure or adds another layer of friction.

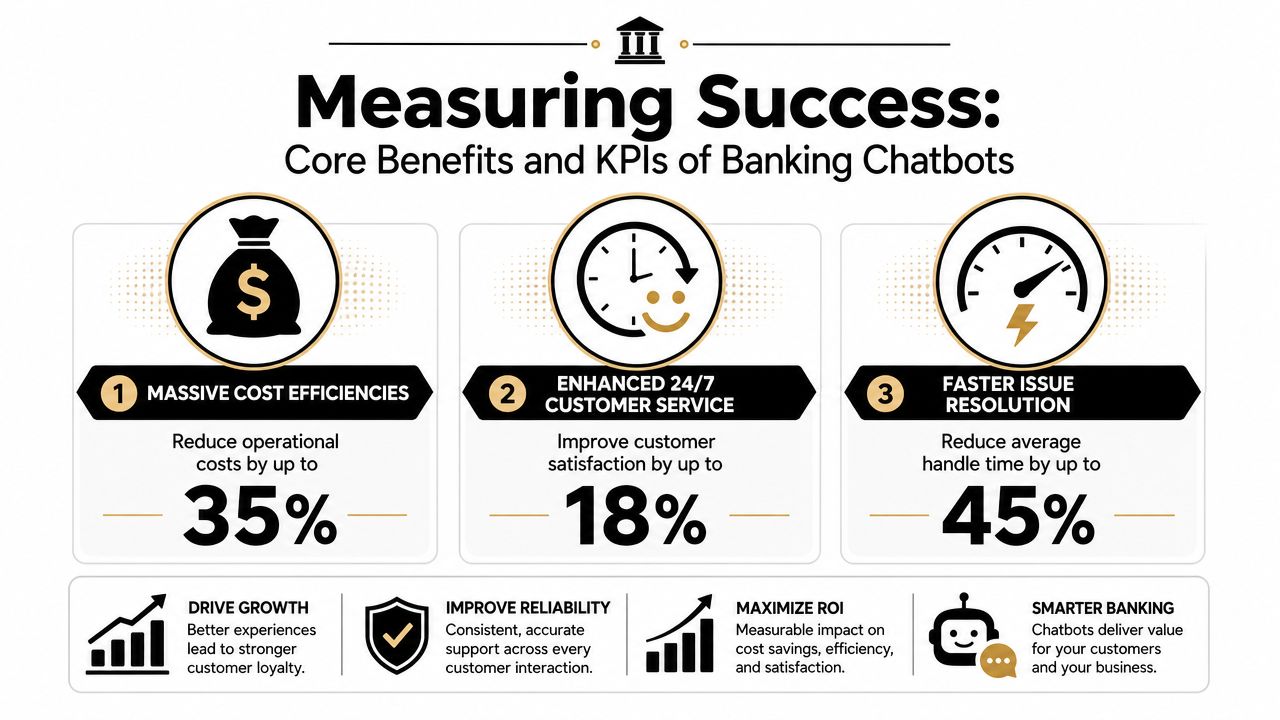

Measuring Success with Core Benefits and KPIs

Banks usually buy into chatbots in banking for three reasons: lower service cost, better customer experience, and the ability to handle more volume without having to add more staff. Each goal needs a different measurement lens.

Cost efficiency that shows up in operations

The easiest promise to understand is cost control. If a bot can resolve routine requests like balance inquiries, card controls, or payment questions, agents spend more time on exceptions and less time on repetitive work.

The mistake is measuring only “number of chats handled.” That can hide a poor experience. Better KPIs include:

- Bot containment rate: The share of conversations the bot resolves without human takeover.

- Cost per resolved interaction: The operating cost of solving the issue, not just replying.

- Escalation quality: Whether handoffs arrive with context, authentication status, and conversation history.

A bank manager should ask a hard question: did the bot reduce work, or did it just move work downstream?

Customer experience that goes beyond speed

Customer experience improves when the customer gets a clear answer quickly and doesn't need to repeat themselves. The quality gap between legacy bots and newer systems is sharp. One industry analysis reports that traditional banking chatbots achieve 29% customer satisfaction, while modern conversational AI reaches 72%, with 65% faster response times and 50% fewer chat abandonments, according to Galileo's analysis of banking chatbot satisfaction.

That tells you something important. Better language models alone aren't the whole story. Banks get stronger outcomes when the system understands context well enough to keep the conversation moving.

Useful customer-facing KPIs include:

- CSAT: Was the customer satisfied with the interaction?

- First contact resolution: Did the customer solve the issue in one session?

- Abandonment rate: Did the customer leave before resolution?

- Time to resolution: How long did it take to finish the task?

If you need a practical framework for tracking these metrics, this guide on AI chatbot KPIs that measure success is a useful reference.

A fast reply isn't the same as a solved problem. In banking, resolution matters more than response.

Operational scalability without service collapse

Scalability sounds abstract until peak periods hit. Think payroll day, fraud spikes, card outage events, or month-end payment traffic. A good chatbot gives the bank a pressure valve. It handles routine demand while routing the complex and urgent cases correctly.

A simple way to monitor this is with a short KPI table:

| KPI | What it tells you |

|---|---|

| Containment rate | Whether the bot actually resolves routine demand |

| FCR | Whether customers get closure in one interaction |

| CSAT | Whether automation feels helpful rather than frustrating |

| Abandonment rate | Whether users drop off before the issue is solved |

| Average resolution time | Whether workflows are getting faster |

The strategic takeaway is straightforward. Success doesn't come from having a chatbot. It comes from having a chatbot that resolves real work.

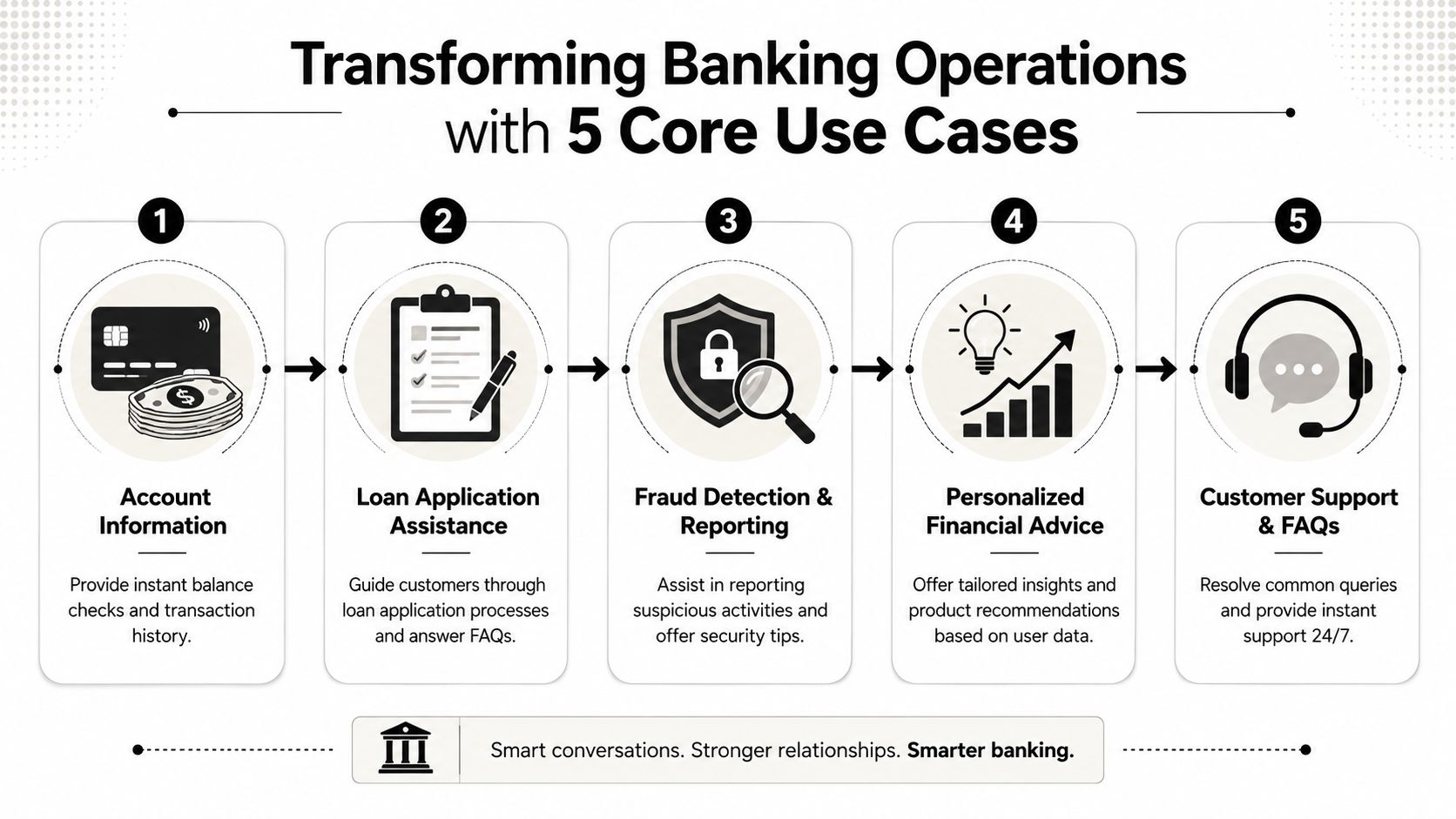

Transforming Banking Operations with 5 Core Use Cases

Five use cases usually separate a basic FAQ bot from a banking assistant that can do real operational work. That distinction matters. A bot that only answers policy questions reduces a small amount of contact center volume. A bot that can verify, guide, trigger, and confirm transactions starts to reshape service delivery.

A practical way to read the examples below is to track the maturity shift. The first use cases answer questions. The later ones complete steps inside the banking journey. For a bank manager, that is the key progression to watch.

Routine account service

This is usually the starting point because the workflow is clear and the customer intent is easy to spot.

A customer asks, “Did my utility payment go through?” or “What is my current balance after yesterday's transfer?” The assistant checks the account data, returns the answer in plain language, and offers a next step if needed. That next step could be viewing recent transactions, downloading a statement, or raising a dispute if the payment failed.

These interactions may look simple, but they build trust. Customers judge a bank on dozens of small moments, not just on major financial decisions. If the assistant handles everyday service accurately, people are more willing to use it for higher-value tasks later.

Onboarding and early application help

Application journeys often break down for a basic reason. The applicant gets confused.

A chatbot can explain what a field means, clarify which document is required, remind the customer what happens after submission, and keep the process moving. It does not replace underwriting or compliance checks. It reduces drop-off caused by uncertainty.

That makes this use case valuable on both sides of the business. Customers get clearer guidance. Operations teams get fewer incomplete applications and fewer repetitive “what does this mean?” calls.

Here's a short explainer that shows how many institutions think about these journeys in practice:

Transfers and payments

This is the point where many banks move from conversational support into assisted execution.

Instead of forcing customers through a maze of menus, the bot can guide a task in plain language. A user says, “Transfer funds from savings to checking,” and the assistant confirms the amount, checks for missing details, and sends the request to the right system. The same pattern applies to bill payments, peer-to-peer transfers, and payment status checks.

For managers, this is a useful dividing line. FAQ bots answer about a process. Transactional assistants help complete the process safely.

That shift also raises the bar for integration. If payment and transfer journeys depend on customer records, permissions, and workflow history, the assistant needs strong links into internal systems. A good starting point is understanding how chatbot CRM integration connects conversation history with customer operations. Banks exploring account aggregation and external payment flows should also understand the benefits of Open Banking APIs, especially where real-time data access affects service design.

Loan and mortgage pre-qualification support

Borrowing products create a different kind of workload. Many customer questions are important but repetitive, especially at the early research stage.

A banking assistant can explain common terms, outline required documents, estimate the next steps in the application process, and help customers prepare before they speak with a specialist. That saves time for lending teams and gives applicants faster orientation.

Restraint still matters here. Process guidance is useful. Product recommendations and financial advice often require a human relationship manager, both for compliance reasons and for customer confidence.

Fraud alerts and suspicious activity workflows

Fraud service is one of the clearest examples of where speed and clarity matter more than conversational polish.

If a suspicious charge appears late at night, customers want three things quickly. Is this transaction real? What should I do now? Is my account safe? A chatbot can handle the first-response workflow by presenting the alert, asking the customer to confirm whether the transaction is recognized, and triggering the next approved action, such as freezing a card or starting a dispute path.

This use case works well because the customer intent is urgent, the process is structured, and the bank can define the permitted actions tightly. In practice, that means shorter delays, faster containment, and less pressure on phone queues during incident spikes.

Across all five use cases, the pattern is consistent. The strongest banking chatbots start with service questions, then expand into guided actions, then support controlled transactions. That evolution matters more than having a long list of features. It shows whether the assistant is becoming part of bank operations.

Understanding Banking Chatbot Architecture and Integration

A banking chatbot sounds complicated until you break it into a simple chain of events. The customer says something. The system figures out what they mean. Then it asks the bank's systems to do something allowed and returns the result.

The waiter and kitchen analogy

Think of the chatbot as a waiter in a restaurant.

The customer says, “I want to lock my card.” The waiter's first job is to understand the order correctly. In chatbot terms, that's the NLP layer, which identifies the user's intent. The waiter's second job is to take the order to the kitchen. In chatbot terms, that's the API orchestration layer, which sends the request into the correct banking system. Finally, the waiter brings back the meal, or in this case, the response and next steps.

That basic flow is why one technical point matters more than many buyers expect. A banking chatbot's real value comes from transaction reliability, not conversational charm. As Backbase explains in its guide to AI chatbots in banking, these systems are built around intent recognition plus API orchestration, and success depends more on secure, low-latency execution than on fluent wording.

What banks need behind the chat window

A non-technical manager can evaluate architecture with a short checklist:

- Identity and authentication: Can the system confirm who the user is before sensitive actions?

- API access: Can it reach core systems for balances, transfers, card controls, disputes, and alerts?

- Idempotency: If a request is retried, will the bank avoid duplicate actions?

- Auditability: Can the bank trace what the bot asked, what the system returned, and what the customer saw?

If your team is reviewing integration options more broadly, this guide on chatbot CRM integration helps frame what clean system connectivity should look like.

Why open banking matters to this design

Many banks still operate with a mix of modern interfaces and older core platforms. That's why APIs matter so much. They act like controlled doorways between the chatbot and the systems that hold account, payment, and customer data.

For teams comparing integration approaches, this overview of the benefits of Open Banking APIs is useful because it explains why standardized access methods can simplify product design and service delivery.

If the chatbot understands the request but can't reach the right system securely, the conversation will still fail.

Navigating Regulation Security and Customer Trust

A banking chatbot can be fast, polished, and available all night. None of that matters if customers don't trust it with sensitive tasks.

That trust problem is real. Fewer than 30% of consumers trust AI chatbots for financial information and advice, according to Banking Dive's reporting on consumer concerns about AI in banking. The same reporting notes that customers show stronger interest in practical, lower-risk help such as alerts that help them avoid fees.

Trust starts with scope, not branding

Banks often try to build confidence with friendly design and reassuring copy. That helps a little. It doesn't solve the core issue.

Customers trust banking automation more when the task is narrow, useful, and easy to verify. A fraud alert, card freeze, transaction lookup, or payment reminder feels concrete. “What should I do with my money?” feels exposed, subjective, and higher risk.

That's why a disciplined rollout matters. Start with transactional support where the user can confirm the result. Expand only after the bank proves reliability, security, and escalation discipline.

Security and compliance are product features

Managers sometimes treat compliance as the legal team's checklist after the product is designed. In banking, that's backwards. Security and compliance shape the product itself.

A well-governed chatbot should support:

- Controlled authentication: Sensitive actions should require the right level of identity verification.

- Data minimization: Only the needed customer data should be exposed in the conversation flow.

- Clear escalation rules: The bot should know when to stop and route to a human.

- Audit trails: Teams need records for review, dispute handling, and internal oversight.

For a practical look at risk controls, this guide to AI chatbot security and data privacy for businesses gives a helpful framework.

Explainability matters more than many teams expect

When a bot answers a branch-hours question, explainability isn't a major issue. When it helps with disputes, disclosures, fraud workflows, or product guidance, it becomes much more important. Staff need to understand why the system responded as it did, what rule or model drove the action, and when a human should intervene.

If you want a concise overview of the supervisory lens on this topic, this summary of key CFPB concerns for banking leaders is worth reviewing.

Customers don't need a bank chatbot to sound human. They need it to behave predictably, protect their data, and know its limits.

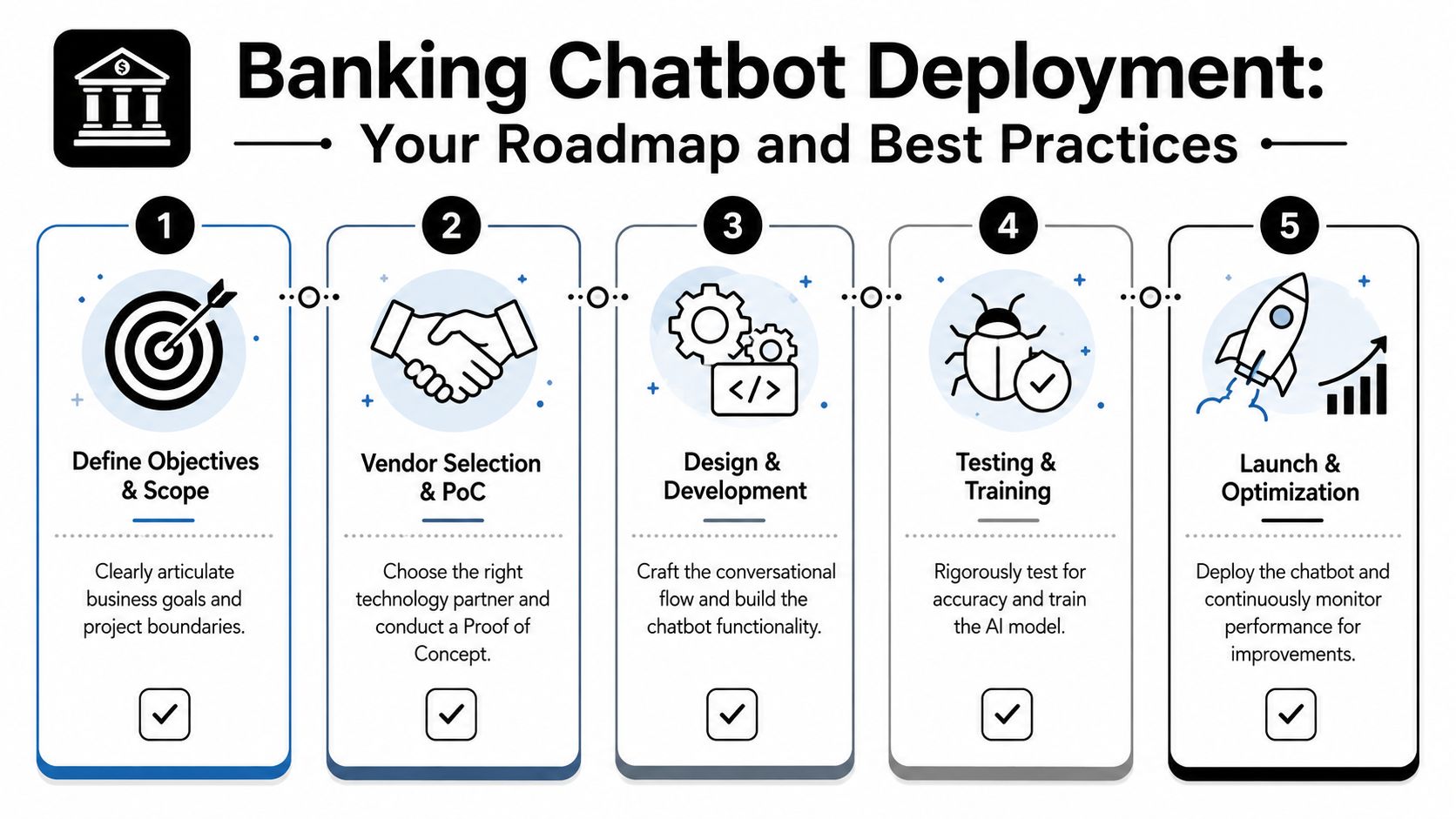

Your Deployment Roadmap and Best Practices

Banks that get real value from chatbots rarely start with the broadest vision. They start with one service task that already happens thousands of times a month, then build outward. That approach matters because a banking chatbot is less like a marketing widget and more like a new front-desk employee. You do not hand a new teller every possible responsibility on day one.

A practical six-step rollout

Choose one high-impact use case

Pick a job that is frequent, rules-based, and easy to measure. Good starting points include card freezes, balance and transaction questions, payment status, branch or ATM lookup, and account servicing requests. Broad financial guidance is usually a poor first launch because it requires more judgment, more controls, and more exception handling.Start in the channel customers already use for service

For many banks, that is the mobile app or secure online banking portal. The logic is simple. If customers already check balances, review transactions, and manage cards there, adding conversational help in the same place reduces friction and keeps authentication easier to manage. As noted earlier, banks also tend to prioritize fraud-related messaging and other secure service workflows in digital channels first.Map the conversation to the actual operating process

A chatbot flow should mirror what the bank can really deliver. If the bot offers help with a dispute, there needs to be a defined intake process, a case status, service-level expectations, and a handoff path when documents or agent review are required. Otherwise, the bot becomes a polite dead end.Integrate core systems before refining personality

Many teams spend weeks polishing wording and greetings while the hard part sits untouched. A banking assistant creates value when it can read account data, trigger approved actions, log the interaction, and pass context to staff. Pleasant language helps. Working connections matter more.Pilot with a narrow audience

Start with one customer segment, one product line, or one internal support team. This gives you a controlled environment to spot failure patterns, tune intent recognition, and verify that escalation works under real conditions. It also lowers operational risk if something breaks.Expand in stages from FAQ bot to transactional assistant

This is the shift many banks underestimate. A basic bot answers questions. A more mature assistant can authenticate the user, complete a card control request, start a dispute workflow, or surface account-specific information inside policy limits. Each stage needs new integrations, tighter testing, and clearer success criteria.

Best practices that separate stable launches from stalled ones

Strong deployments usually share the same operating habits.

- Design handoff as part of the product: The bot should transfer the case with conversation history, customer context, and the reason for escalation.

- Use plain language: Customers should know whether they are getting information, starting a request, or completing an action.

- Test edge cases early: Failed login attempts, duplicate submissions, vague questions, and system outages reveal more than happy-path demos do.

- Review conversation logs on a set schedule: Transcript reviews show where customers hesitate, where wording creates confusion, and where backend steps are slowing the experience.

- Give operations staff ownership: Product, service, compliance, and frontline teams all need a say. Chatbots fail when they are treated as a side project owned only by digital or IT.

One more point often gets missed. Success is not the launch date. Success is the point at which the bot handles a meaningful share of routine work accurately enough that staff time can shift to higher-value cases.

Pilot first, then expand

The safest pattern is simple. Prove one workflow, then add the next adjacent job.

For example, a bank might begin with balance questions and card lock requests. Once those flows are reliable, it can add dispute intake, payment reminders, or authenticated account servicing. That progression turns the chatbot from a searchable FAQ layer into an integrated service assistant. It also creates a cleaner path for vendor evaluation later, because you can judge providers on what they must support next, not just what they can demo today.

The strongest banking chatbot programs do not grow because the first version sounded impressive. They grow because the first version worked.

Choosing Your AI Partner A Vendor Selection Checklist

Vendor selection is where many chatbot projects drift off course. A polished demo can hide weak controls, shallow integrations, or vague implementation support. In financial services, you need to evaluate the provider the way you'd evaluate any critical infrastructure partner.

Security and compliance questions

These questions belong at the top of the list, not buried at the end.

| Evaluation Area | Key Question to Ask |

|---|---|

| Security and Compliance | How does your platform authenticate users before sensitive actions? |

| Security and Compliance | What audit logs do you provide for conversations, system actions, and handoffs? |

| Security and Compliance | How do you control access to customer data across teams and environments? |

| Security and Compliance | How does the system support data retention, deletion, and policy enforcement? |

| Security and Compliance | What is your process for handling incidents, model updates, and governance review? |

A strong vendor should answer these clearly, without vague reassurance. If the provider can't explain how it handles identity, logs, permissions, and change control, move on.

Technical capability questions

A banking chatbot lives or dies by integration quality. Ask how the platform connects to core systems, card services, CRM tools, and knowledge bases.

Use questions like these:

- Intent handling: How does the platform recognize customer intent when wording is messy or incomplete?

- System orchestration: Can it trigger secure workflows such as balance checks, card controls, transfers, and dispute intake?

- Fallback behavior: What happens when the system can't classify the request confidently?

- Human escalation: Can it hand off with conversation context, customer state, and action history intact?

- Channel support: Can the same logic work consistently across app, web, and messaging channels?

Ask vendors to show the failure path, not just the happy path. That's where platform quality becomes obvious.

Business support and implementation questions

Even technically strong platforms can fail if the provider disappears after kickoff.

A practical shortlist should include questions such as:

- Implementation model: Who configures workflows, tests integrations, and supports launch?

- Training process: How do they help your team refine intents, responses, and governance rules?

- Reporting: What analytics do managers get on containment, escalation, and unresolved themes?

- Change management: How are new use cases added without destabilizing existing flows?

- Commercial clarity: Is pricing easy to understand, or does cost rise unpredictably with usage and customization?

The right partner won't just sell software. They'll help your bank design a service model that works under real operating pressure.

If you want a simpler way to launch AI chat without a long development cycle, Hyperleap AI gives teams a no-code platform to answer questions, capture leads, and stay available around the clock across website and messaging channels. It's a practical option for businesses that want fast deployment, grounded responses, and one place to manage conversations without building everything from scratch.